Learn how to choose a benefits broker in the UK, key red flags to avoid, and whether you need one. Plus, a modern alternative to brokers and spreadsheets.

.png)

.png)

.png)

Selecting a benefits broker is one of the highest-impact decisions your HR or People team will make. But here's the question most companies skip: do you actually need a traditional broker? This guide walks through how to evaluate brokers if you decide you need one. It also introduces the modern alternative that's replacing the broker-platform-HRIS fragmentation model entirely.

Most UK companies approach benefits the same way: hire a broker to procure core benefits, layer on a platform for administration, then manually coordinate everything with your HRIS and payroll. It's the accepted model.

But just because it's common doesn't mean it's optimal.

Before diving into broker selection criteria, let's examine what you're actually signing up for with the traditional model, and whether it still makes sense in 2026.

Traditional brokers earn commission from insurers when they place your business. Typically, between 10-15% for health insurance and 15-20% for pensions, then a 3-5% fee on top. On a £200,000 annual health insurance bill, that's £26,000 to £40,000 going to a broker who, based on customer feedback, often "speaks to them once a year."

This isn't necessarily unfair. Brokers do provide value. But the question is whether that value matches the cost and whether there's a better way to get the same (or better) outcomes.

The traditional broker model creates 3 specific pain points that compound over time:

You're managing separate relationships with your:

Because each system operates independently, data flows manually between them via spreadsheets and CSV uploads. When an employee joins, leaves, or changes salary, you're updating information in multiple places. Or you’ll discover weeks later that someone's coverage never got cancelled.

Many companies experience the same painful cycle: the broker provides renewal quotes 3 days before the deadline, premiums have jumped 15-30%, and you're forced to make rushed decisions without adequate time to compare alternatives or properly shop the market. The broker controls the timeline. You react.

After the initial placement, what exactly are you getting for that 3-5% commission? Some brokers provide excellent ongoing support. Many don't. Customer research consistently surfaces the same complaint: "I pay them all year but only hear from them at renewal." If your broker relationship feels extractive rather than supportive, that's a signal.

Despite these challenges, traditional brokers remain the right choice for certain organisations:

If these describe your situation, the guidance below will help you select the best broker. But if you're a scaling small-to-mid-market company drowning in manual admin, constantly reconciling spreadsheets, and frustrated by the broker-platform-HRIS juggling act, there's now a better way.

Before we get into broker selection criteria, it's worth understanding what's changed in the benefits market over the past few years.

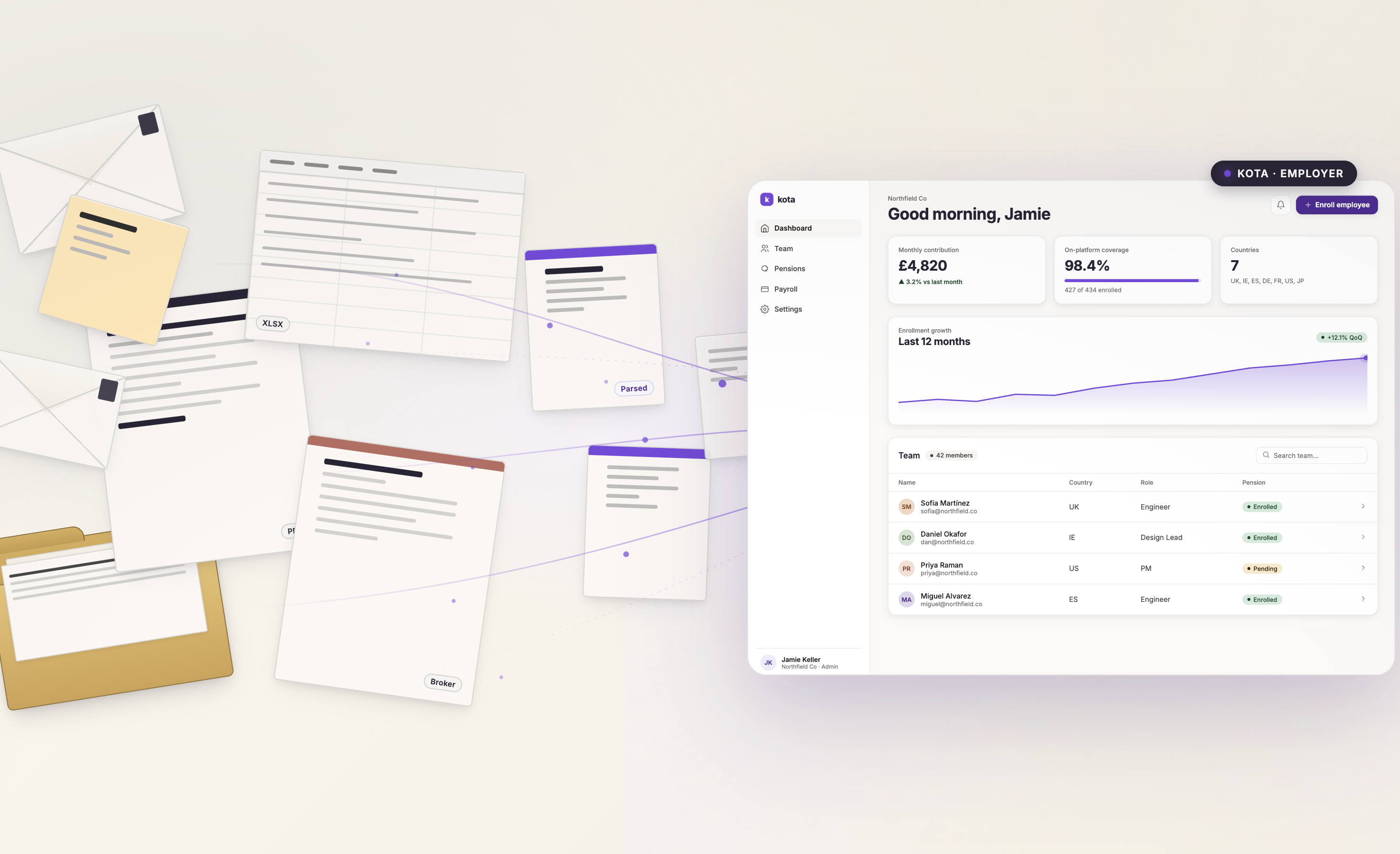

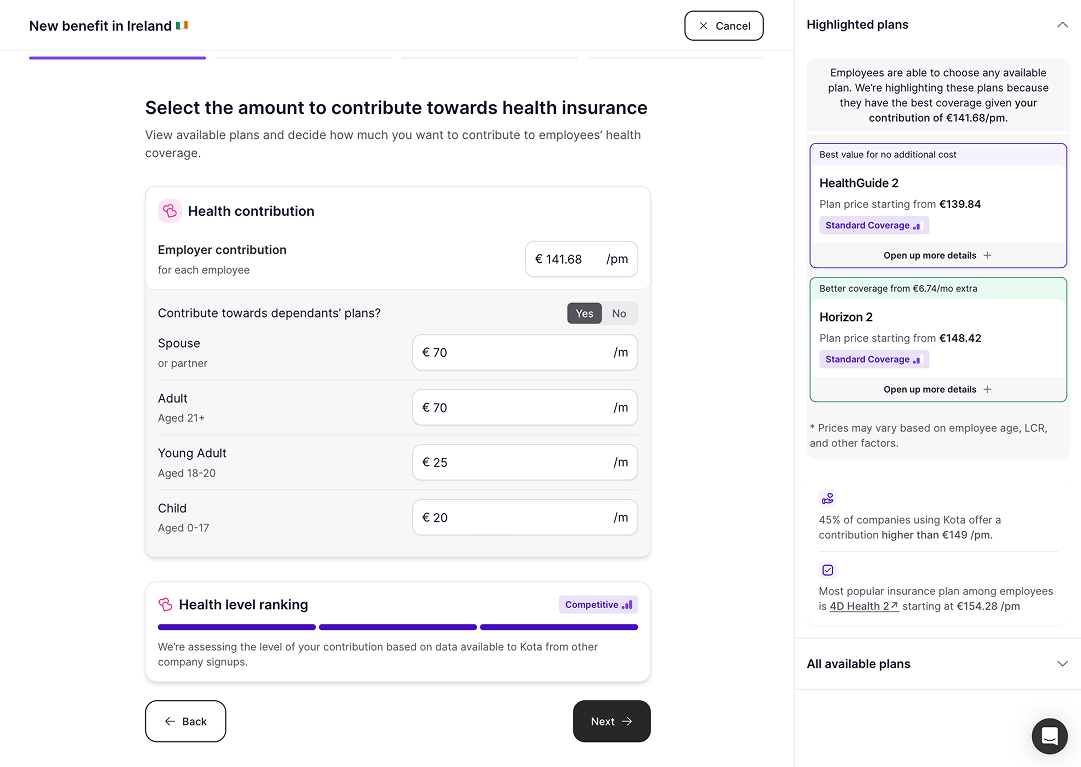

A new category has emerged: platforms like Kota that are also FCA registered insurance brokers. (Kota is registered as an Appointed Representative with the FCA) These platforms handle both procurement and administration in a single unified system, with direct integrations with insurers and pension providers. Instead of coordinating 3 separate vendors, you have a single system that automatically syncs from HRIS to end providers and back to payroll.

Kota pioneered this approach in the UK and Ireland.

Kota is a next-gen employee benefits platform built to take the complexity of running benefits off your plate and replace it with something simpler, smarter and genuinely engaging for employees.

It handles the entire benefits journey end-to-end, from HRIS integration through to provider management. Instead of juggling separate portals for pensions, health insurance and flexible benefits, your team manages everything in one place.

For employees, it’s just as seamless. Core and flexible benefits are accessed through a clean, intuitive app, with the option of a benefits spend card for added flexibility and everyday perks.

The result? You avoid paying for both a broker and a platform whilst eliminating the manual coordination work between them.

For many UK and Irish SMEs, it's a fundamentally simpler, more efficient model than the traditional three-party broker-platform-HRIS setup.

Now, if you still feel a traditional broker is your best option, here's how to select one properly.

Most companies don't actually shop for brokers. They receive referrals from other businesses or stick with their insurance provider's recommendation.

This is a mistake.

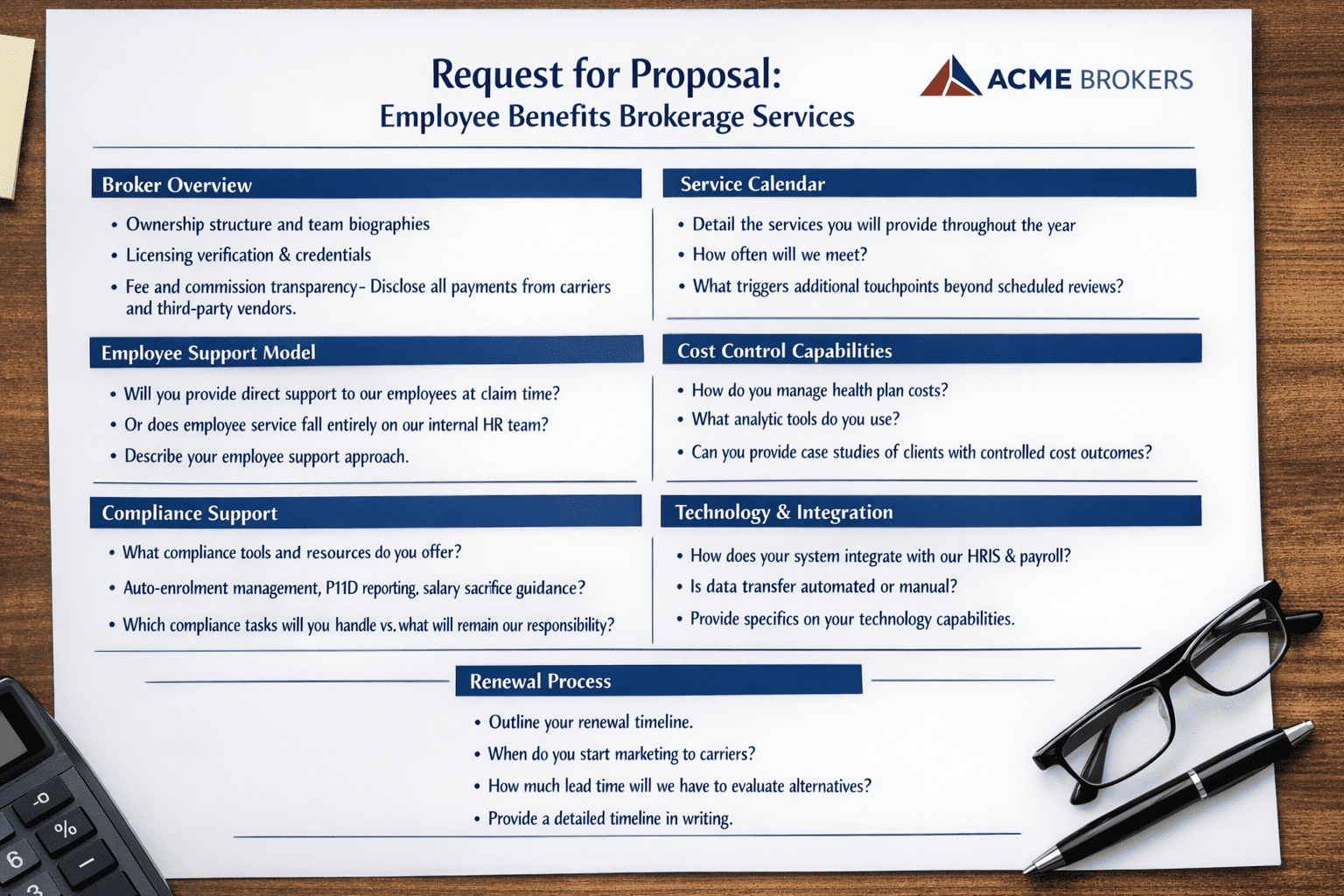

Interview at least 3-5 candidates to understand the range of capabilities, approaches, and service models available. Look for brokers who:

Pay attention to how brokers describe their service model. Do they talk about annual touchpoints, or do they describe an ongoing strategic partnership? The language reveals their approach.

Don’t assume they can assess brokers through conversation alone.

A well-structured RFP helps you clarify what you actually need. It also requires prospective brokers to clearly document what they’ll deliver. It’s not just about reducing the decision to a spreadsheet comparison. After all, personality and cultural fit still matter in your relationship with a broker.

Having documented responses ensures you’re comparing capabilities objectively rather than relying on impressions alone.

Review RFP responses systematically. Create a scoring rubric across the key categories above. Look for specifics, not platitudes. "We provide excellent service" means nothing. "We conduct quarterly business reviews, provide monthly reporting on claim trends, and guarantee 24-hour response times on compliance questions" is measurable.

Narrow your candidate pool to 2-3 finalists based on this scoring. These are the brokers you'll invest significant time meeting with.

Schedule substantive meetings with each finalist. These should be working sessions, not sales pitches. Bring specific scenarios from your business:

Watch how they respond. Are they defensive? Do they acknowledge industry problems whilst explaining how their approach differs? Can they show examples of solving similar challenges for other clients?

Finalist interviews also reveal cultural fit. You might work with this broker for years. Do they feel like partners or vendors? Do they listen, or just pitch?

Before making a final decision, speak with at least 3 current clients of your finalist brokers. Don't just accept the references the broker provides. Ask for clients similar to your size and industry, then do your own research to find others.

Key questions for references:

Once you've selected a broker, document everything. Get a formal services agreement outlining deliverables, communication cadence, fees/commissions, and performance expectations. Request a Business Associates Agreement, privacy policy, and commission transparency statement.

Keep all these documents in a secure location along with your RFP, scoring sheets, and interview notes. When it's time to review performance in 18-24 months, you'll want this record.

Certain warning signs should disqualify broker candidates immediately:

Following all 5 steps above requires significant time and effort. You're essentially conducting a major procurement exercise. And even when done well, you're still left managing the broker-platform-HRIS fragmentation that creates so much ongoing work.

Before investing weeks in broker selection, ask yourself: do we actually need a traditional broker, or is there a simpler model that eliminates this entire coordination challenge?

For many UK and Irish scaling companies, the answer is increasingly clear. Modern benefits infrastructure, like Kota, removes the fragmentation that makes traditional benefits management so painful. You get broker-level expertise built into the platform. Direct provider integrations that sync automatically. Transparent per-employee pricing without commission surprises.

And most importantly, you eliminate the constant manual work of updating employee data across multiple disconnected systems.

If this approach interests you, explore whether a modern, automated platform that combines licensed brokerage with technology might be a better fit than assembling and coordinating multiple vendors.

Your employees deserve great benefits. Your People team deserves simple tools that actually remove work rather than creating more. And your finance team deserves predictable costs without hidden broker fees.

The good news? With Kota, you can have all three.

Book a demo to see how Kota replaces brokers, platforms, and spreadsheets with one unified system.

Trevor Gardiner QFA, RPA, APA in Insurance. With 23 years of experience in Financial Services, I have a strong passion for Health Insurance and Pensions.

.png)

.png)

.svg)

.svg)

.svg)