This is a living guide. Kota's Health Benefits Lead, Charlie, guides you through a four-part video series to help UK and Irish employers navigate group health insurance renewals with confidence — from pre-renewal prep all the way to day-to-day policy management. We'll be publishing each module here as new episodes drop. Bookmark this page and come back for more.

.png)

.png)

.png)

With Charlie, Health Benefits Lead at Kota

Most employers find group health insurance renewal harder than it should be, and that's before you factor in the specific quirks of the Irish and UK markets. The process is time-consuming, the documentation is dense, and the people on the other side of the table do this every day while you do it once a year.

In this first module, we cover why renewals consistently feel so chaotic, what a well-run renewal actually looks like, and the three different ways employers typically manage the process.

The renewal period causes dread for a lot of HR managers, finance leads, and founders - whether you're managing a group scheme with VHI, Laya, or Irish Life Health in Ireland, or navigating a PMI policy with Bupa, AXA Health, or Vitality in the UK. A few different pressures tend to hit at once.

Renewing a health insurance policy takes far more time than it should. There's the back-and-forth with providers, the chase for the right documentation, the effort of getting employee data into the right format for your payroll system, and the general cognitive weight of trying to understand what you're being presented with. If you're also managing Benefit-in-Kind (BIK) implications in Ireland, or ensuring your P11D reporting is accurate in the UK, the administrative load compounds further. It eats into your calendar at the worst possible time - usually when you have a hundred other priorities competing for your attention.

Insurance providers and brokers do this every single day. You don't. That asymmetry matters because renewals are often presented in ways that make the process feel more complex than necessary - reinforcing the idea that you need them to navigate it. You're handed dense documentation, technical jargon, and comparison tables that are difficult to interpret without prior context.

In Ireland, the market operates under community rating - meaning everyone on the same plan pays the same premium regardless of age or health status. That's consumer-friendly in principle, but it also means the differences between VHI's PMI plans, Laya's Inspire or Connect schemes, and Irish Life Health's offerings are subtle and genuinely hard to decode without expertise. In the UK, PMI underwriting adds another layer of complexity - whether you're on moratorium underwriting, Full Medical Underwriting (FMU), or Continued Personal Medical Exclusions (CPME) affects what your employees are actually covered for, and many employers don't fully understand the distinction until a claim is declined.

The result is that most employers make decisions with incomplete information, or defer entirely to whoever is in front of them.

Group health policies have a lot of moving parts: different levels of hospital cover, outpatient benefit limits, excess options, mental health provisions, dental and optical add-ons, employee eligibility rules. In the UK, this is compounded by the need to decide how your PMI scheme sits alongside NHS entitlements - a conversation that often goes unaddressed. Keeping all of that in your head while also evaluating whether you're getting good value is a lot to ask of anyone.

And underpinning all of this is a very real pressure: these decisions matter for your people. Getting it wrong isn't just a cost issue. It affects whether your employees feel supported, whether they actually use their benefits, and whether they value what you're providing them.

The goal isn't just to get the renewal done. It's to come out the other side with a policy that works for your business and your team - without it consuming weeks of your time. Here's what that looks like in practice.

A well-run renewal shouldn't require a drawn-out, painful process. The heavy lifting - understanding your policy, tracking claims, monitoring employee feedback - should happen continuously throughout the year so that when renewal time comes, you're already prepared. We'll come back to how to build that cadence in later modules.

In both the UK and Ireland, premiums have been rising. In Ireland, VHI, Laya, and Irish Life Health have all implemented price increases in recent years, with some plans going up by double digits. In the UK, average SME PMI premiums have been climbing steadily. The temptation to treat renewal as a cost-cutting exercise is understandable, but cutting the premium by switching to thinner cover rarely serves anyone well.

A more useful lens is value: how accurately is your employee data being maintained, is the cover actually being used, and do the benefits on offer match what your workforce needs? A plan that costs slightly more but is actively used and understood by your team will almost always deliver more than one that sits in a welcome pack and never gets touched.

A health insurance policy that's hard to use might as well not exist. If your employees don't understand their cover, can't easily access their benefits, or don't hear about the policy until something goes wrong, they won't value it - regardless of how comprehensive the plan actually is. This is as true in Dublin as it is in London or Manchester. A good renewal process treats employee experience as a key success metric, not an afterthought.

A group health insurance renewal isn't a single moment in time - it's the culmination of a year-round process. We break it down into three distinct phases:

This is your preparation window. In the two to three months before your policy is due to renew, you should be pulling together everything you need: updated and accurate employee data, any feedback you've gathered from staff throughout the year, and a clear picture of how the policy has been used. In Ireland, this is also a good time to review your BIK obligations and check that your records align with what your provider has on file. In the UK, it's the moment to review your claims history and consider whether your underwriting basis still makes sense.

The more prepared you are at this stage, the smoother the actual renewal will be.

This is when you receive your renewal documentation, review your new premium, and make decisions about cover changes or provider switches. With the right groundwork in place from the pre-renewal phase, this period becomes a decision-making exercise rather than a scramble to understand the basics.

In Ireland, this is the window to compare across VHI, Laya Healthcare, and Irish Life Health - and potentially Level Health, which has been gaining ground with competitive corporate plans. In the UK, this is when Bupa, AXA Health, Aviva, and Vitality should all be in the mix for comparison, and when independent advice on underwriting terms can make a material difference.

This is the phase most employers underinvest in - and the one that makes the biggest difference. Day-to-day policy management includes adding new joiners, removing leavers, processing claims, and keeping a running record of how the policy is performing. In practice, this is where most of the administrative pain lives: employee turnover, mid-year changes, incorrect data, and poor record-keeping are the primary reasons renewals feel so chaotic when they come around.

The notes and data you gather throughout the year become the intelligence you need when renewal comes around again.

Most companies in the UK and Ireland manage their group health insurance in one of three ways - and the approach you choose has a real bearing on how much work the renewal is, and how well-informed you are when it counts.

Going direct means no middleman, no additional advisory fees, and a single point of contact. If you're only managing one benefit and want simplicity, this can work well - particularly for smaller businesses dealing directly with a provider like VHI or Bupa.

The downside is that you're entirely dependent on one provider's perspective. You have no visibility into the wider market, and no independent check on whether you're getting good value. When your VHI, Laya, Irish Life, Bupa, or AXA renewal lands with a significant premium increase, you have no context for whether that's in line with the market or not - and the provider has little incentive to tell you.

A broker gives you a broader view of the market. They can pull quotes from multiple providers across both countries, help you compare cover levels, and advise on which policy might suit your team best. In Ireland, a good broker will be able to navigate the nuances between corporate plan tiers across the three main providers. In the UK, they'll help you understand the right underwriting basis for your workforce.

What a broker typically won't do is help you manage the policy day-to-day. Once the contract is signed, you're usually handed back to the provider directly, and the broker reappears at renewal time when it suits them to keep the relationship going. There's also the question of incentive alignment - some brokers have preferred providers they're commercially motivated to recommend, which doesn't always serve your best interests.

We built Kota to combine what's best about both of the above. Available to employers in both Ireland and the UK, our platform handles the day-to-day administrative work that typically falls on HR: adding new joiners, removing leavers, processing claims, and keeping employee data accurate and up to date. For Irish employers, that means cleaner BIK records and fewer payroll headaches. For UK employers, that means accurate P11D data and a clear picture of who's on the scheme at any given time.

On the advisory side, we provide the kind of independent, market-wide guidance you'd expect from a good broker - with clear, jargon-free explanations of what's available, what the differences actually mean, and what will suit your team. No preferred providers, no opaque commission structures.

The result is a single place to manage your company health insurance, with people who know the Irish and UK markets inside out and no conflicts of interest.

This first module sets the foundation. In the modules ahead, we go deeper on each phase of the renewal journey - what to look for when comparing providers in Ireland and the UK, how to evaluate your current policy's performance, and how to have better conversations with whoever is managing your insurance on your behalf.

Speak to the Kota team if you want to explore how we can help you take control of your next renewal.

In module one, we looked at why health insurance renewals feel so difficult: the time cost, the knowledge gap, and the pressure of knowing these decisions matter for your people. This module is about the first of the three stages we outlined, the pre-renewal period, and how getting this right makes everything that follows significantly easier.

The core idea: preparation does more for you than negotiation ever will. Walking into a renewal with your data in order means you're telling the market what you need, rather than the other way around. And if you've been on a group scheme for at least a year, you already have everything you need to do that well.

The most common mistake employers make at renewal time is leading with the premium. Costs are going up, and it's tempting to treat renewal as a cost-cutting exercise, but it tends to produce worse outcomes than starting from a different question.

Why premiums keep rising (and won't stop anytime soon)

Premiums across both the UK and Irish markets have been rising steadily and that trend isn't going to reverse. The main drivers are:

Expecting an annual increase and planning for it is more useful than treating it as a surprise each year.

The better question to ask

Rather than "how do I get the price down?", the more useful frame is: am I getting the right cover for what we're paying? A policy with strong, relevant benefits your team actually uses will always represent better value than a cheaper one they don't understand or can't access easily.

You're not starting from scratch

If you've had a group scheme for a year or more, you have real intelligence to work with:

Most employers don't draw on this as much as they could. That's the gap preparation closes.

The first thing to look at before renewal isn't your policy documents. It's your people. Workforce demographics shift, and benefits that were a good fit a year ago might not be the right fit now.

Questions to ask about your team

Each of these changes can affect which benefits your team will actually use and value, and should factor into what you're looking for at renewal.

Practical implications by market

Before you can decide what you want from your next policy, you need to understand clearly what you have. This sounds obvious, but a lot of employers are less familiar with their current policy than they realise, often because it was set up some time ago and hasn't been reviewed properly since.

The key areas to get clear on

By market

Claims data is one of the most valuable inputs you have at renewal, and it's consistently misread.

The common mistake

When employers see high usage in a particular benefit area, the instinct is often to cut it to bring costs down. The logic runs the wrong way.

How to actually read it

High usage is evidence that a benefit is working. Low usage is where you look for savings. This moves the exercise from cost-cutting to optimisation, building a policy that fits your workforce rather than simply a cheaper one.

Claims data tells you what people used. Complaints and shortfalls tell you what people wanted and couldn't get. Together they give you a much more complete picture.

Where this feedback tends to live

These aren't always formal complaints. They're often quiet frustrations:

Look for this feedback in:

Running a pre-renewal survey

A brief survey asking your team what they valued, what they missed, and what felt hard to use doesn't need a high response rate to be useful. A handful of consistent responses will tell you a lot. And having that feedback in hand changes the quality of the conversation you can have with a provider when it's time to negotiate.

Pulling all of this together before renewal starts is what puts you in control of the conversation.

Your renewal brief should include:

Going into renewal with this brief means you're presenting your requirements rather than responding to whatever you're offered. You know which benefits are non-negotiable. You know where the current policy is falling short. You know what's changed. You're in a much stronger position.

The goal is to keep this folder updated throughout the year rather than assembled in a rush, so that when renewal arrives, you're already prepared.

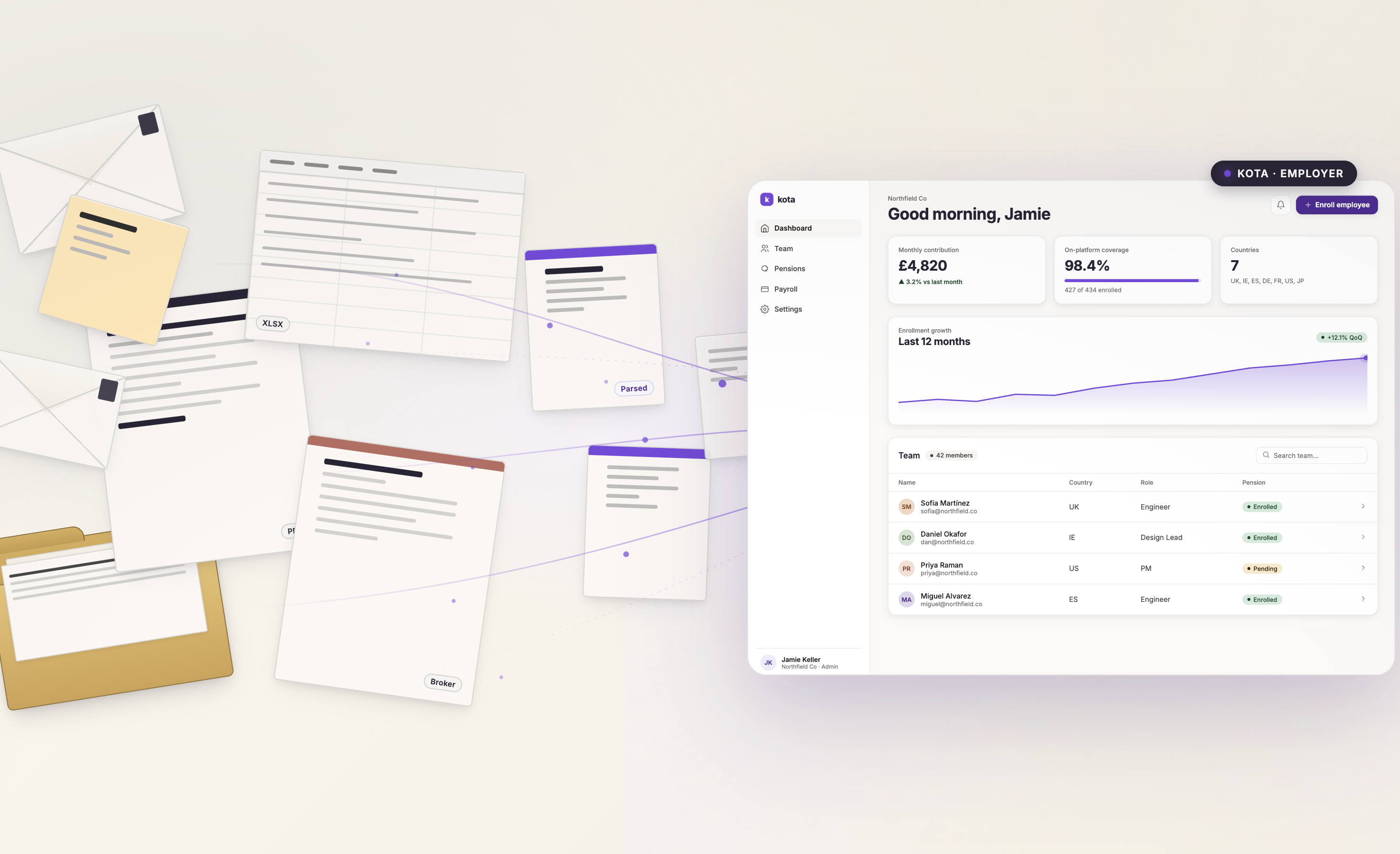

With Kota, none of this needs to be compiled manually. Your dashboard holds your claims usage, employee data, and renewal information in one place, updated throughout the year as your team changes, so that when the pre-renewal period begins, everything is already there.

We've also put together a free pre-renewal checklist covering the key things to have in order before your renewal lands. Download it here if you want a practical starting point.

In module three, we go into the active renewal period itself: how to compare what's on the market, what to look for in a new quote, and how to know whether staying with your current provider actually makes sense.

Charlie Blake is Kota's Health Benefits Lead, helping employers in Ireland and the UK get more out of their group health insurance — at renewal and throughout the year.

.png)

.png)

.svg)

.svg)

.svg)